Layer 3 Scaling Solutions

Layer 3s have been garnering a lot of attention in the Ethereum community recently. These scaling solutions offer a number of benefits over their Layer 2 counterparts, including higher levels of customizability and optimization, the use of recursive proofs, and the ability to settle on an L2.

Recursive proofs are a type of validity proof that combines multiple proofs into a single, more compact proof. This not only reduces the number of proofs that need to be verified on the Ethereum main-chain (L1), but also results in lower latency since statements can be proven in parallel.

Layer 3s are better suited for adopting validity proofs rather than fraud proofs, as fraud proofs require a challenge period for transaction withdrawals, which goes against the goal of L3s to transact and settle more quickly and cheaply.

Several protocols are currently working on L3 solutions, including StarkWare, zkSync, Immutable, and Sorare. These protocols offer various benefits for developers, such as the ability to build decentralized applications (dApps) on EVM-compatible L3s, access to liquidity through a cross-rollup liquidity layer, and the ability to build on an L3 while still inheriting a level of Ethereum’s security.

While L3s have a number of pros, including more customizability and higher throughput, they are also harder to build and have low adoption so far, with limited developer tooling.

Overall, it's clear that Layer 3s have the potential to be a monumental upgrade to Ethereum's scalability, but only time will tell if they will live up to their promise.

Liquity Protocol

Mesopotamian cuneiform tablets are humanity's oldest remnants of written communication. These tablets contain ledger entries, which suggests that borrowing and lending have been around since the beginning of written history. It's not clear whether these ancient transactions also involved interest rates, but it's possible.

Now, on to more modern financial innovations: the Liquity Protocol is a decentralized, collateralized debt position (CDP) protocol that allows users to take out interest-free loans in $LUSD (the native, dollar-pegged stablecoin) using ETH as collateral. The minimum collateralization ratio (MCR) is 110%, meaning that users must deposit at least 110% of the value of their loan in ETH to secure it.

The process of taking out a loan on the Liquity Protocol is similar to that of the MakerDAO protocol, in which users can mint a dollar-pegged stablecoin using a volatile cryptocurrency as collateral. However, there are two key differences: first, ETH is the only acceptable collateral on Liquity, and second, losses are safeguarded differently.

To mint $LUSD on Liquity, users must first open a "trove" (essentially a digital vault) and deposit ETH as collateral. They can then redeem $LUSD in increments of at least $2,000, but must pay a one-time borrowing fee (ranging from 0.5% to 5%) and a liquidation reserve of $200. The liquidation reserve is used to cover gas costs in the event that a user's trove is liquidated (more on that later), and is fully refundable if the trove is not liquidated.

Repaying $LUSD is as simple as depositing it back into the trove. Users can choose to partially or fully close their collateralized debt position by repaying their debt.

If a trove's collateral value falls below the MCR, the trove is liquidated and the collateral is transferred to a "stability pool" to be distributed among stability providers. These providers essentially act as a backstop for the protocol, compensating lenders in $LUSD when borrowers default on their loans. In exchange for their services, stability providers are rewarded with the seized ETH collateral and additional rewards in the $LQTY token.

$LQTY is a utility token that allows holders to earn a portion of the fees generated by loan issuance and $LUSD. These fees are paid out in both $LUSD and ETH. $LQTY can also be staked to earn a share of these fees. There is a fixed maximum supply of 100 million $LQTY, and the tokens are distributed according to a yearly halving schedule: 32,000,000 * (1–0.5^year). This issuance curve is intended to incentivize early adopters while also maintaining long-term incentives.

One interesting aspect of the Liquity Protocol is that it has no official front-ends (websites or apps that allow users to interact with the protocol). Instead, the team behind Liquity incentivized community developers to build their own front-ends and charge whatever percentage of the liquidation fee they wanted. As a result, the market has settled on a 1% fee.

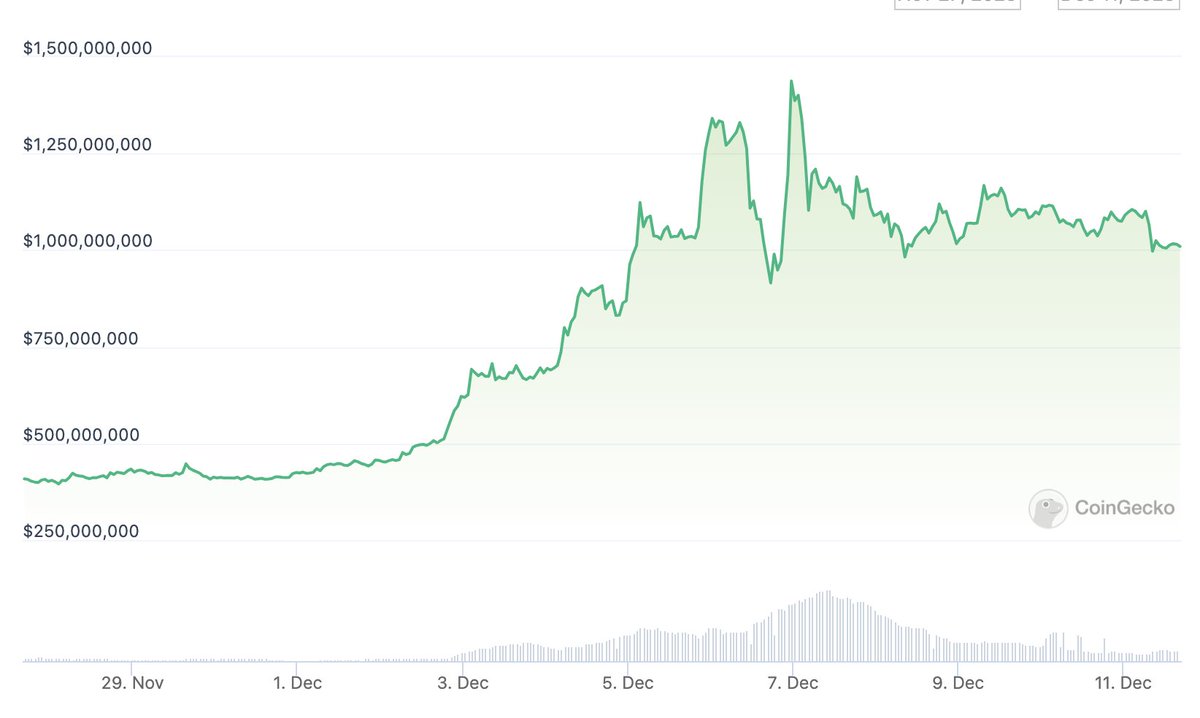

Despite its innovative structure and strong community support, the Liquity Protocol has struggled to maintain its $LUSD peg and its total value locked (TVL) has fallen from a high of $4.5 billion to around $430 million today. This may be due to a lack of liquidity for large trades and the fact that the staking yield on Liquity is roughly equivalent to that of regular ETH staking. It's worth noting that many high-risk crypto projects have seen their TVL

Sources:

https://www.theblockresearch.com/an-overview-of-layer-3s-182539

https://vitalik.ca/general/2022/09/17/layer_3.html

Layer 3 Scaling Solutions

Layer 3s have been garnering a lot of attention in the Ethereum community recently. These scaling solutions offer a number of benefits over their Layer 2 counterparts, including higher levels of customizability and optimization, the use of recursive proofs, and the ability to settle on an L2.

Recursive proofs are a type of validity proof that combines multiple proofs into a single, more compact proof. This not only reduces the number of proofs that need to be verified on the Ethereum main-chain (L1), but also results in lower latency since statements can be proven in parallel.

Layer 3s are better suited for adopting validity proofs rather than fraud proofs, as fraud proofs require a challenge period for transaction withdrawals, which goes against the goal of L3s to transact and settle more quickly and cheaply.

Several protocols are currently working on L3 solutions, including StarkWare, zkSync, Immutable, and Sorare. These protocols offer various benefits for developers, such as the ability to build decentralized applications (dApps) on EVM-compatible L3s, access to liquidity through a cross-rollup liquidity layer, and the ability to build on an L3 while still inheriting a level of Ethereum’s security.

While L3s have a number of pros, including more customizability and higher throughput, they are also harder to build and have low adoption so far, with limited developer tooling.

Overall, it's clear that Layer 3s have the potential to be a monumental upgrade to Ethereum's scalability, but only time will tell if they will live up to their promise.

Liquity Protocol

Mesopotamian cuneiform tablets are humanity's oldest remnants of written communication. These tablets contain ledger entries, which suggests that borrowing and lending have been around since the beginning of written history. It's not clear whether these ancient transactions also involved interest rates, but it's possible.

Now, on to more modern financial innovations: the Liquity Protocol is a decentralized, collateralized debt position (CDP) protocol that allows users to take out interest-free loans in $LUSD (the native, dollar-pegged stablecoin) using ETH as collateral. The minimum collateralization ratio (MCR) is 110%, meaning that users must deposit at least 110% of the value of their loan in ETH to secure it.

The process of taking out a loan on the Liquity Protocol is similar to that of the MakerDAO protocol, in which users can mint a dollar-pegged stablecoin using a volatile cryptocurrency as collateral. However, there are two key differences: first, ETH is the only acceptable collateral on Liquity, and second, losses are safeguarded differently.

To mint $LUSD on Liquity, users must first open a "trove" (essentially a digital vault) and deposit ETH as collateral. They can then redeem $LUSD in increments of at least $2,000, but must pay a one-time borrowing fee (ranging from 0.5% to 5%) and a liquidation reserve of $200. The liquidation reserve is used to cover gas costs in the event that a user's trove is liquidated (more on that later), and is fully refundable if the trove is not liquidated.

Repaying $LUSD is as simple as depositing it back into the trove. Users can choose to partially or fully close their collateralized debt position by repaying their debt.

If a trove's collateral value falls below the MCR, the trove is liquidated and the collateral is transferred to a "stability pool" to be distributed among stability providers. These providers essentially act as a backstop for the protocol, compensating lenders in $LUSD when borrowers default on their loans. In exchange for their services, stability providers are rewarded with the seized ETH collateral and additional rewards in the $LQTY token.

$LQTY is a utility token that allows holders to earn a portion of the fees generated by loan issuance and $LUSD. These fees are paid out in both $LUSD and ETH. $LQTY can also be staked to earn a share of these fees. There is a fixed maximum supply of 100 million $LQTY, and the tokens are distributed according to a yearly halving schedule: 32,000,000 * (1–0.5^year). This issuance curve is intended to incentivize early adopters while also maintaining long-term incentives.

One interesting aspect of the Liquity Protocol is that it has no official front-ends (websites or apps that allow users to interact with the protocol). Instead, the team behind Liquity incentivized community developers to build their own front-ends and charge whatever percentage of the liquidation fee they wanted. As a result, the market has settled on a 1% fee.

Despite its innovative structure and strong community support, the Liquity Protocol has struggled to maintain its $LUSD peg and its total value locked (TVL) has fallen from a high of $4.5 billion to around $430 million today. This may be due to a lack of liquidity for large trades and the fact that the staking yield on Liquity is roughly equivalent to that of regular ETH staking. It's worth noting that many high-risk crypto projects have seen their TVL

Sources:

https://www.theblockresearch.com/an-overview-of-layer-3s-182539

https://vitalik.ca/general/2022/09/17/layer_3.html

Continue reading

Continue reading

Layer 3 Scaling Solutions AND Liquity Protocol

Nov 25, 2022

Layer 3 Scaling Solutions AND Liquity Protocol

Nov 25, 2022